Full Charge Ahead: Why CLN Energy Could Be India’s Next Battery Breakout

With surging revenues, improving return metrics, and a strong foothold in the booming EV and stationary power segment, CLN Energy is a microcap powertrain story ready to scale.

Executive Summary

Powering India’s EV Future

One Battery Pack at a Time CLN Energy Ltd. is a vertically integrated lithium-ion battery manufacturer targeting India’s fast-growing EV and renewable energy markets. Founded in 2019, the company has compounded revenue at over 60% YoY, improved capital efficiency, and maintained a clean balance sheet. Well-positioned to ride the EV adoption curve, CLN delivers B2B battery systems, electric motors, and integrated energy solutions for both mobility and stationary use cases. At ~₹504/share and a ~₹530 Cr market cap, CLN trades at ~41x P/E and 5.9x P/B—pricing in growth but still cheaper than many EV sector peers. With strong momentum, upcoming export orders, and strategic capital deployment, CLN could emerge as a next-gen compounder in India’s SME energy tech space over the next 3–5 years.

Business Description

CLN Energy designs, assembles, and sells lithium-ion batteries, electric motors, and energy management systems for electric vehicles (2W/3W/4W) and stationary uses like solar and telecom.

Core Competency:

Custom B2B battery packs (LFP/NMC chemistries)

EV powertrains and BLDC motors

Strong in-house R&D

ISO-certified manufacturing in Uttar Pradesh

Industry Overview & Competitive Positioning

India’s EV and energy storage market is expected to exceed ₹1 lakh crore by 2030, driven by electrification of transport and solar adoption.

Growth Drivers:

FAME II + state EV subsidies

Rising fuel costs and demand for last-mile mobility

Telecom and solar sectors seeking grid independence

CLN’s Positioning:

Low-cost, custom B2B solutions

Tier 2/3 vendor partnerships

Rapid scale from ₹133 Cr to ₹220 Cr in one year

Optionality:

US/Europe export orders initiated in FY25

Platform-based powertrain solutions for OEMs

The Growth Story So Far

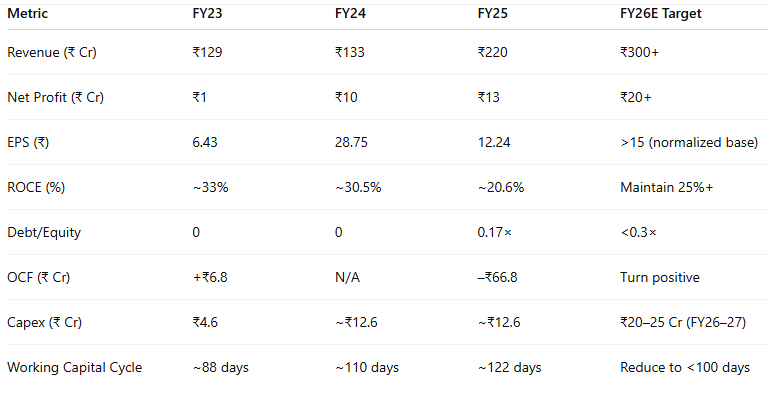

Strong Financial Performance (FY25):

Revenue: ₹219 Cr (+66% YoY)

PAT: ₹13 Cr (+32%)

EPS: ₹12.24

ROE: 24% (down from 73% peak in FY24)

ROCE: 30.5%

Balance Sheet:

Debt/Equity: 0.17×

Negative Operating Cash Flow: ₹(67 Cr) due to increased receivables and inventory

Capex Spend: ₹13 Cr (R&D + scaling)

Fresh Funds: ₹83 Cr via preferential issue (Apr 2025)

Working Capital Cycle: ~122 days

Debtor Days: ↑ from 88 to 125

CLN Energy Integrated Value Chain

Key Takeaways:

CLN Energy adds value from design to delivery, excluding raw cell manufacturing.

Focused on high-margin system integration, not commoditized cell production.

Owns 4 out of 5 critical stages, enabling product flexibility, cost control, and IP development.

The business model resembles a tech-focused tier-1 supplier, not a generic assembler.

Strategic Catalyst—Export Orders & R&D-Led Scale

In early 2025, CLN secured a $5 million export order for custom battery systems to the Middle East and Europe, marking its first international footprint.

Meanwhile, new investment in battery lab R&D, automated pack assembly, and BLDC motor development aims to future-proof margins and capacity.

If executed well, this shift from assembler to tech-driven integrator could expand both revenue and valuation multiples.

Investor Takeaway

CLN Energy offers a rare mix: high revenue growth, asset-light operations, and future-facing products, all while maintaining capital efficiency.

While working capital drag and cash burn are near-term headwinds, FY26 could show free cash flow reversal if scale and receivables normalize.

At ~41x earnings, this isn’t cheap, but the valuation reflects potential, not hype. Think long runway, not quick flips.

Q4 FY25 Concall Highlights

Growth Guidance: 35–40% YoY sales growth targeted for FY26

Export Strategy: Repeat orders expected from 3 overseas clients

Capex Plan: ₹20–25 Cr over FY26–27 for automation and testing

Margins: Steady 9% EBITDA margin with intent to reach 12%

Challenges: Receivable delays and increased credit cycles with OEM clients

Monitoring Dashboard

Valuation Context

CLN Energy trades at approximately 41× FY25 earnings and 5.9× book value, which may appear elevated at first glance. However, in the context of India’s energy transition and EV supply chain build-out, this valuation reflects growth pricing, not irrational exuberance.

To put this in perspective:

Despite its smaller scale, CLN’s ROCE is comparable to larger peers, and its topline growth (+66% YoY) surpasses most listed competitors. While Servotech commands a P/E of ~75× with similar revenues but lower returns, CLN’s better capital efficiency and export potential justify its valuation.

Conclusion:

CLN’s 41× P/E reflects the market’s confidence in its future trajectory — supported by strong fundamentals, niche product innovation, and growing strategic relevance. If execution stays on track, the valuation could compress over time as earnings catch up, offering potential for both re‑rating and earnings-led compounding.

Investment Case & Risks

Bull Case:

Revenue crosses ₹300 Cr with stable 10–12% margins

Export orders repeat and scale

The working capital cycle normalizes

R&D investment translates to better pricing/margins

Bear Case:

Receivable pressure impacts cash flow again

Execution delays in export or R&D productization

Margins stagnate due to rising input/operational costs

Valuation derates if FY26 misses growth/margin targets

Contribute whatever feels right to you; your support motivates us to create more valuable content

Highlights & Risks

Strengths

Strong growth: Revenue rose ~66% YoY, with net profit up 32%.

High capital efficiency: ROCE above 20%.

Low debt burden: Debt-equity ratio remains conservative.

Innovative, scalable business model: targeting EV and solar segments.

Risks

No dividends paid: Entirely growth-focused, no shareholder payouts.

High receivables: Working capital tie-up is a growing concern.

Valuation appears stretched: a P/E of 41× and a P/B of 5.9× imply a premium.

Profitability volatility: ROE and margins have fluctuated, particularly after a strong FY 2024.

Promoter Holding: ~72.6% (as of March 2025)

No pledged shares

Founder-led with focus on reinvestment over dividends

Final Word

CLN Energy is not just another battery assembler; it’s becoming a vertically integrated powertrain tech player in a sunrise sector.

If it executes on margin scaling, exports, and R&D-led innovation, the market may soon rerate it into a ₹1,000 Cr+ story.

Disclosure & Disclaimer

This is not investment advice. All views are personal and for educational purposes only. Always consult a financial advisor before investing.

Enjoyed this deep dive? Tap the like to boost discovery!

Comments are open below. Share your take or challenge ours.

Follow us on X & LinkedIn

Join Finance Fusion for exclusive insights & stock discussions.

This is going to give easy 10x

Yes, we can say