This Tiny Energy Company Has Massive Gas Optionality

But Its Future Depends on One Critical Trigger

There are companies that generate steady cash flow.

And then there are companies that hold hidden optionality.

Prabha Energy Ltd belongs to the second category.

For years, investors ignored the company because:

Revenue was small,Profitability was inconsistent and Execution was slow

But recently, attention has started to build.

Not because of current earnings.

Because of potential production.

This is not a conventional growth story.

This is an execution-driven energy optionality story.

The Business in One Line

Prabha Energy operates in:

Coal Bed Methane

Unconventional gas exploration

Energy resource development

The company holds interests in gas-bearing coal blocks where methane can be extracted and sold as fuel.

This is not a consumer business.

This is a resource monetization business.

Why Investors Are Suddenly Watching This Company

Because the company controls energy assets that could become valuable once production scales.

In energy exploration, valuation is not driven by current revenue.

It is driven by:

Reserves

Production capacity

Future cash flow

If production starts, the business transforms.

If production delays continue, the story stalls.

That is the entire investment thesis.

The Core Assets

Where the Real Value Lies

The company holds stakes in multiple coal bed methane blocks.

The most important ones include:

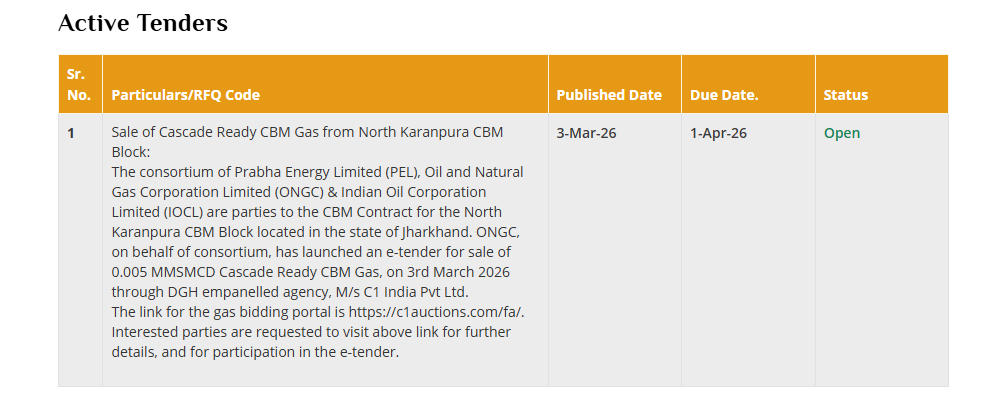

North Karanpura block

Jharia block

These regions contain mature coal seams capable of producing methane gas.

And methane demand in India is rising.

Why This Sector Matters Now

India is pushing aggressively toward domestic energy production.

Because:

Energy imports are expensive

Gas demand is rising

Energy security is becoming critical

Coal bed methane is part of that strategy.

And companies holding reserves are positioned to benefit.

The Real Growth Engine: Commercial Gas Production

This is the single most important trigger.

Not announcements.

Not exploration.

Not reserves.

Production.

Once gas production begins at scale:

Revenue increases rapidly

Operating leverage kicks in

Cash flow improves

Valuation expands

Without production, none of this happens.

The Financial Reality

The Numbers Investors Must Understand

This is not a profitable company yet.

Revenue remains extremely small.

Recent trend:

Low revenue

Irregular profitability

Negative operating leverage

This is the reality of early-stage energy companies.

They invest first.

They generate revenue later.

Most wealth is built before the story becomes obvious. Paid members get access at that stage. Unlock high-conviction ideas before they play out.

The Balance Sheet

Survival Capacity Matters Here

The company maintains:

Moderate cash reserves

Limited debt

Ability to fund operations

This is critical.

Because energy projects require capital.

And companies without funding fail before production begins.

Why Investors Are Betting on This Story

There are three structural reasons.

1. Resource Optionality

Energy companies are valued on potential production.

Not current profit.

If reserves are monetized:

Revenue scales quickly

Margins improve dramatically

Valuation re-rates

2. Scarcity of Listed CBM Players

Very few listed companies operate in:

Coal bed methane

Unconventional gas

Scarcity creates investor attention.

3. Energy Transition Tailwind

India is moving toward:

Cleaner fuels

Domestic gas production

Reduced import dependency

This supports long-term demand.

The Risk Section

What Investors Must Watch Closely

This is a high-risk business.

Execution risk is the biggest variable.

1. Production Delays

If projects take longer than expected:

Revenue stays low

Cash burn continues

2. Funding Risk

Energy projects require continuous capital.

If funding is insufficient:

Dilution risk increases.

3. Commodity Price Risk

Gas prices fluctuate.

Lower prices reduce profitability.

4. Regulatory Risk

Energy extraction requires approvals.

Delays can slow project timelines.

The Real Question

Not:

Will the company announce projects?

But:

Will the company produce gas?

Because production determines everything.

What Could Trigger the Next Re-Rating

These are the key catalysts.

Commercial gas production

Reserve certification

Strategic partnerships

Government policy support

Any one of these can change the valuation trajectory.

Valuation Reality Check

Current valuation reflects:

Future expectations

Not current earnings

This is important.

Because expectations create volatility.

My View

This is not a compounder today. This is an optionality bet.

The upside depends entirely on execution.

If production scales:

The stock can re-rate significantly.

If execution delays continue:

Returns remain limited.

Why I Am Tracking This Company

Because the setup is binary.

Either:

Production begins and valuation expands

Or:

Delays continue and growth stalls

There is very little middle ground.

Bottom Line

This is not a stable earnings business.

It is not a predictable compounder.

It is a:

High-risk energy optionality story

Where execution will determine returns

And in this type of business:

Production is everything.

Interesting Read! Thankyou

use can this in AI data centers?