Zodiac‑JRD‑MKJ Ltd.: A Small-Cap Gem or Value Trap?

Ticker: ZODJRDMKJ Sector: Gems & Jewellery Market Cap: ₹65 Cr Stage: Turnaround Play/Speculative Value

Company Snapshot

Zodiac-JRD-MKJ Ltd., a Mumbai-based micro-cap, is in the jewelry manufacturing and trading business—dealing in gold, diamond, and semi-precious stone pieces. With a legacy dating back to 1987, the company is thinly traded, largely under the radar, and now testing diversification through a plastics venture.

Financial Snapshot

Revenue & Margins

FY25 revenue jumped 81% YoY to ₹22.99 crore, a rare bright spot in its otherwise slow growth track record (3-year CAGR of ~6.4%).

Operating margins have been volatile, peaking near 17% in Q3 FY24 but dipping into negative territory in other quarters.

EBITDA margin currently stands around 2.9%, indicating limited operating leverage.

Profitability

FY25 net profit came in at ₹0.43 crore, a turnaround from a ₹1.37 crore loss in FY24.

Return on Equity (ROE) is weak at approximately 0.64%.

Profit margins remain thin and inconsistent.

Cash Flow & Working Capital

Debtor days are alarmingly high at 297 days, suggesting a stretched working capital cycle.

Inventory levels are also significant, tying up additional cash.

Balance Sheet Highlights

Promoters hold about 30%, a figure that has seen some decline in recent years.

The company has minimal debt, offering a cushion against interest rate hikes or liquidity shocks.

Book value is notably higher than the current market cap, reflecting potentially undervalued assets.

Recent Catalyst: Strategic Diversification

On July 1, 2025, Zodiac acquired a 90% stake in VEM Plastic Molding, signaling a pivot from its core jewelry business into the plastic manufacturing segment. This move could reduce industry concentration risk or distract from an already challenged core. Execution is critical.

“We are evaluating opportunities to expand our footprint across value-added plastic components alongside jewellery packaging.”

— FY25 Annual Report

Market Valuation

The stock trades in the range of ₹57–59, off from its 52-week high of ₹84.80.

With a TTM EPS of ₹1.00, the P/E ratio is steep at ~55x, raising questions about valuation justification.

The P/B ratio is low, around 0.43–0.53, suggesting undervaluation relative to book value.

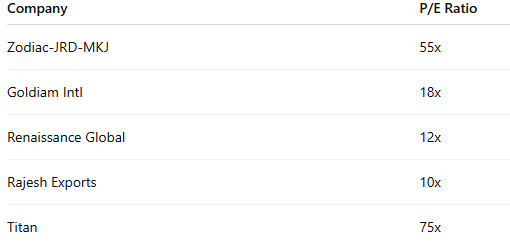

P/E Ratio Comparison

The market is pricing Zodiac at a premium compared to peers, despite its weaker fundamentals:

Who’s Behind the Wheel?

Management includes long-time promoters with deep industry connections but limited visibility and investor engagement. Promoter holding (~30%) has declined recently, which can signal strategic repositioning or disinterest.

Management Commentary

“We are evaluating opportunities to expand our footprint across value-added plastic components alongside jewellery packaging.”

— FY25 Annual Report (Paraphrased)

Recent Development: Strategic Diversification

On July 1, 2025, the company acquired a 90% stake in VEM Plastic Molding, a move that signals diversification into the plastic products space. This could be an attempt to de-risk its jewelry-focused model or to tap into synergies with an entirely new vertical. However, the success of this strategic shift remains to be seen.

Strengths vs Risks

Strengths:

Strong revenue recovery in FY25

Low leverage and healthy balance sheet

Low price-to-book ratio

Risks:

Weak and inconsistent profitability

High working capital requirements

Low return on capital

Valuation appears rich relative to earnings

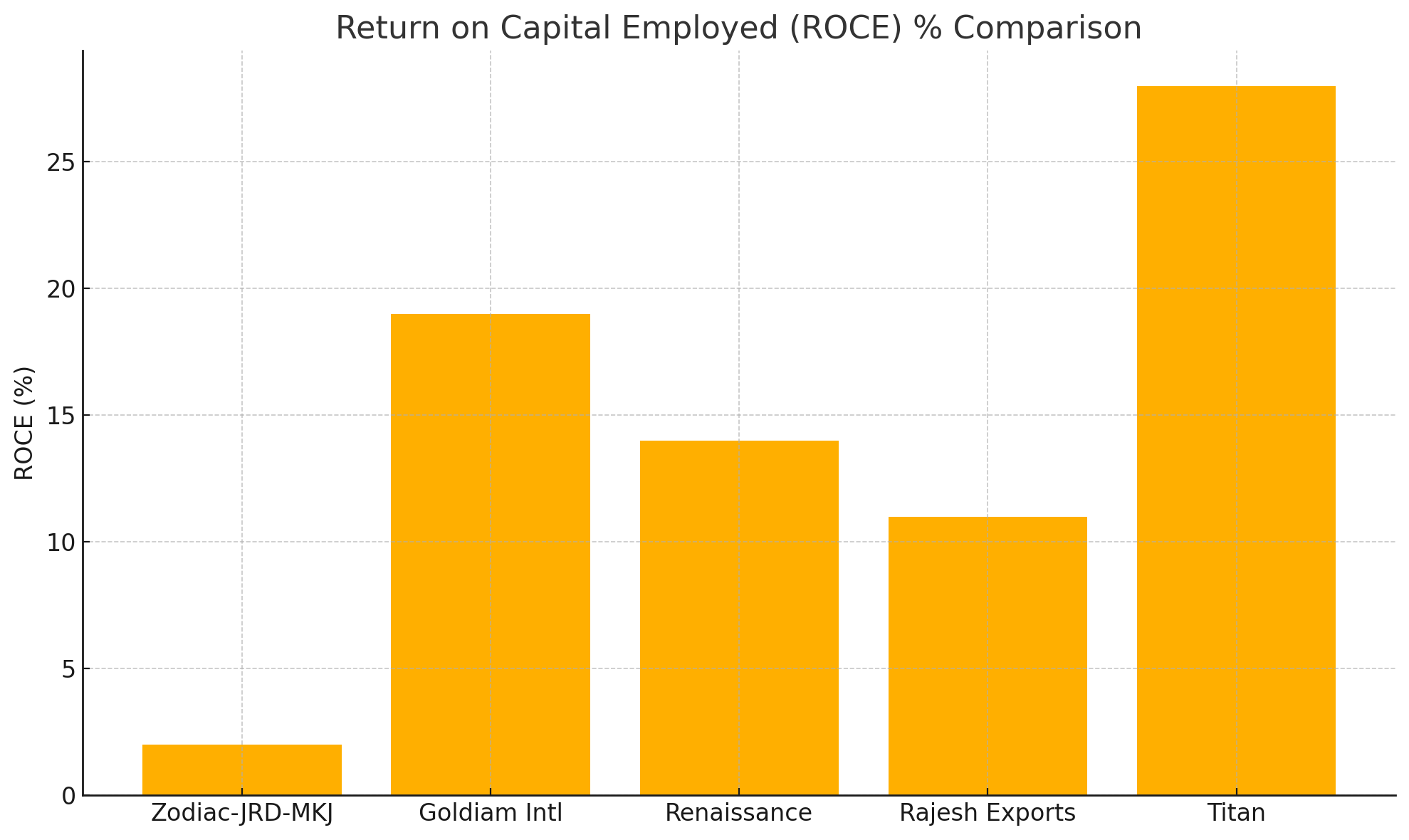

ROCE Comparison

Zodiac’s return on capital is significantly below peers, which questions the sustainability of current valuations:

Investment Outlook

Zodiac-JRD-MKJ is a classic small-cap case: thinly traded, volatile, and loaded with both potential and pitfalls. The recent acquisition could be a meaningful catalyst—if executed well. But investors should remain cautious until the company demonstrates consistent earnings, tighter working capital management, and improved returns.

Key Watchpoints

Q1 FY26 results post-VEM acquisition

Any meaningful reduction in debtor days and inventory

Margin expansion or cost-control initiatives

Promoter activity or further strategic partnerships

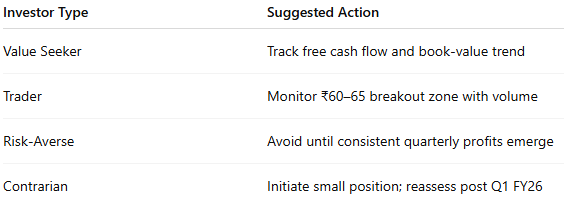

If you're a...

Your support helps keep this research independent. If you’d like to contribute, feel free to donate; any amount helps.

Final Thoughts

Zodiac-JRD-MKJ Ltd. is a speculative turnaround story. It shows flashes of potential with FY25 growth and diversification, but fundamentals remain weak. For now, it’s best suited for micro-cap specialists who understand risk and timing.

Verdict: Worth watching, but tread with caution.

Enjoyed this deep dive? Tap the like to boost discovery!

Comments are open below. Share your take or challenge ours.

Follow us on X & LinkedIn

Join Finance Fusion for exclusive insights & stock discussions.